Why operating partners with the highest-performing portfolios are digitizing spend optimization—and how to do it in 30 days.

Private equity has always required discipline. But the discipline required today is categorically different from what it was a decade ago.

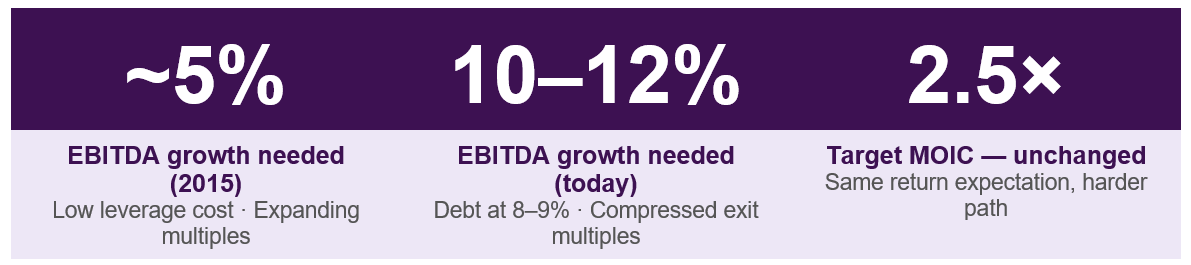

Bain & Company’s Global Private Equity Report 2026 puts the shift in stark arithmetic: to deliver a 2.5× multiple on invested capital over a five-year hold period, portfolio companies that once needed to grow EBITDA by roughly 5% per year must now grow it at 10–12%. Debt is more expensive. Leverage ratios are lower. Exit multiples are flat. The old formula—buy, apply a little discipline, wait for multiple expansion—no longer closes the gap.

The phrase circulating among operating partners is blunt: “12 is the new 5” It captures, in three words, why so many value-creation playbooks are being rewritten right now.

EBITDA growth expectations have doubled from ~5% to 10–12%, while return targets remain unchanged, increasing pressure on portfolio performance.

Claymore Partners’ March 2026 analysis, The Gathering Storm, reinforces the point from a different angle. Five-year rolling distributions as a share of total PE AUM have fallen to record lows. Around $3.6 trillion in unrealized value sits across approximately 29,000 unsold companies. Holding periods are extending. In that environment, the levers that create genuine EBITDA improvement—not accounting adjustments, not narrative—have become the ones that determine which firms raise their next fund.

“The growth that used to be nice-to-have is now existential.” — Bain & Company, Global Private Equity Report 2026

The Levers Are Well Known. The Problem Is Sequencing.

Most operating partners have a standard toolkit: revenue growth, pricing optimization, headcount rationalization, working capital improvement, and procurement cost reduction. All of them work. But they do not all work at the same speed, and they do not all carry the same implementation risk.

Revenue growth requires market conditions to cooperate. Pricing changes risk customer friction and churn if misjudged. Headcount reductions take time, carry legal and cultural complexity, and can damage the capability base that makes the business valuable. Working capital improvements are meaningful but bounded.

Procurement sits in a different category. A dollar saved on the cost of goods and services flows directly to EBITDA. It requires no new customers, no market share gains, and no organizational restructuring. It is operational improvement in its purest form—and in a portfolio company with $50M–$1B in revenue, where goods and services typically represent 60–80% of revenue, the scale of the opportunity is significant.

The SMB Procurement Gap Is Larger Than Most Firms Realize

Portfolio companies in the $50M–$1B revenue range face a structural disadvantage in procurement that their enterprise counterparts do not. Large corporations have dedicated procurement teams, enterprise software platforms, and the negotiating leverage that comes from aggregated spend across hundreds of locations. SMB portfolio companies have none of these.

The result is predictable. On average, SMB portfolio businesses pay approximately 20% more for goods and services than enterprise peers purchasing equivalent categories from the same supplier base. That premium does not represent superior quality or service. It represents the absence of process, visibility, and leverage.

Across a portfolio business with $60M in addressable spend, a 20% price disadvantage represents around $12M in annual overpayment. Even capturing half of that through disciplined procurement improvement delivers 6–7 percentage points of EBITDA improvement. For a business trading at an 8× multiple, every $1M of annualized savings generates approximately $8M in enterprise value.

The operating partners who understand this arithmetic have stopped treating procurement as a support function and started treating it as a value-creation lever—one that, unlike many others, can be activated quickly.

Top-performing PE firms are generating 3 or more additional EBITDA percentage points from procurement. Most firms are not.

Why Traditional Tools Fail the SMB Portfolio Company

The gap persists not because operating partners are unaware of it, but because the available tools have not been well-suited to SMB portfolio companies. The options on offer have historically been three:

- Build internal procurement capability. A dedicated team, hire costs of $600,000 or more, a 12-18-month ramp, and a function that cannot be shared across portcos. Slow, expensive, and not scalable.

- Deploy enterprise eProcurement software. Platforms like Coupa or SAP Ariba carry per-seat and implementation costs designed for businesses ten times the size of a typical portfolio company. The ROI rarely justifies the investment at the SMB scale.

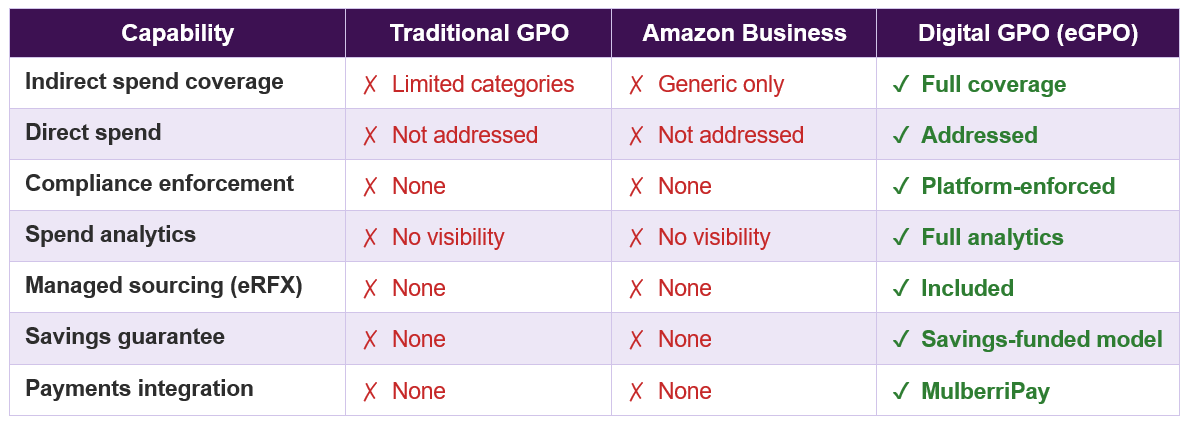

- Use a traditional Group Purchasing Organization (GPO) or Amazon Business. These cover 10–20% of spend at best—typically indirect categories like office supplies and MRO basics. They address none of the high-value direct spend that drives the most material savings opportunities, and they provide no spend analytics or compliance enforcement.

All three approaches share a common flaw: they were designed for a different problem. SMB portfolio companies need enterprise-grade procurement outcomes—spend visibility, category leverage, digital workflows, managed sourcing across both direct and indirect spend—without enterprise complexity or enterprise price tags.

What the Best-Performing Portfolios Do Differently

The PE firms generating 3+ EBITDA percentage points from procurement share a consistent set of practices. They are not more disciplined in any abstract sense. They have simply instrumented the function differently.

- Spend visibility before savings targets. They begin with a full-portfolio spend map—what is being bought, from whom, at what price—before setting savings expectations. Even with ‘dirty’ source data, analysis pin points opportunities. Without this, sourcing activity is speculative and savings claims are unverified.

- Cross-portfolio leverage. They negotiate collectively, not company by company. The GPO model applied at portfolio scale can deliver 7–12% savings across both direct and indirect categories.

- Digital P2P workflows. They replace manual purchasing processes with automated purchase-to-pay systems that cut source-to-pay costs by 30–40% and enforce supplier compliance by default.

- Outcome-based models. They structure procurement partnerships around savings delivery, not software ownership. Where savings guarantees are available, adoption becomes a near-zero-risk decision.

Digital GPO platforms outperform traditional GPOs and Amazon Business by delivering full spend coverage, analytics, compliance, and guaranteed savings.

The Case for Digital GPO: A New Category of Procurement Infrastructure

The emergence of digital Group Purchasing Organization (digital GPO) platforms has created a third path for operating partners—one that did not meaningfully exist until recently. The model combines the buying leverage of a traditional GPO with the analytics, workflow automation, and sourcing capability of an enterprise procurement platform, at a price point sized for SMB portfolio companies.

A digital GPO platform—Mulberri’s eGPO is an example of this model—addresses spend that traditional GPOs and Amazon Business do not reach. Managed sourcing (eRFX) covers high-value direct spend categories such as raw materials, specialist components, and freight, as well as complex services. Spend analytics provides a real-time view across the entire portfolio. Payments integration via a Mastercard-backed system eliminates the accounts-payable inefficiencies that accumulate inside manual purchasing environments.

The model is designed to be operational within 30 days, with no IT project and no capital expenditure. Savings underwrite provisions—where the platform guarantees a minimum savings outcome—remove the adoption risk that has historically caused operating partners to defer procurement initiatives in favor of shorter-cycle improvements.

From Theory to P&L: What Verified Results Look Like

Across 38 sourcing events spanning three portfolio companies—manufacturing, industrial/MRO, and chemicals—addressing $30M in total spend with verified annualized savings of $3M (10%) delivered. Category-level results ranged from 3% on large-volume resins to 49% on specialist direct components and 35% on technical gases.

A separately documented portco case study recorded a program that reached breakeven within eight weeks, with year-one average savings of 12% and a 4× ROI. By year two, average savings had settled at 9% with a 6× ROI as additional spend categories were brought into scope. Headcount savings from the elimination of tactical purchasing and accounts-payable roles added to the financial improvement, alongside a 30% reduction in source-to-pay costs.

For a $100M portfolio company with $60M in spend and a starting EBITDA of $10M, a conservative 5% saving on the first $20M of addressable spend delivers $1M of additional EBITDA. At an 8× multiple, enterprise value rises from $80M to $88M on the back of a single year of procurement improvement.

Procurement optimization delivers measurable results, including $3M in verified savings and up to 6× ROI across portfolio companies.

The Fee Model: Savings-Funded, Not Software-Priced

One of the structural barriers to procurement adoption in PE portfolios has been fee models that require upfront commitment before a single dollar of savings has been realized. The digital GPO model inverts this. ROI estimates below use a conservative 7% average savings assumption across a three-year period:

Savings-funded procurement models generate strong ROI and significant enterprise value uplift across all eGPO plans.

A savings underwrite provision sits beneath each plan, guaranteeing minimum outcomes and removing the financial risk from the adoption decision. The operating partner’s exposure is limited; the upside is direct-to-EBITDA.

The Operating Partner’s Decision

Claymore Partners’ Gathering Storm makes an observation that applies directly to procurement: advice without authority is theatre. The operating partner who identifies a procurement opportunity but lacks the tooling to deliver it at scale across a portfolio is in an advisory position, not an operational one.

In the current PE environment, where holding periods are extending, exit windows are tighter, and EBITDA growth requirements have doubled, that distinction matters. The firms that are closing their next fund are demonstrating systematic value creation—documented savings, verified EBITDA uplift, and repeatable processes that can be deployed across a portfolio, not on a case-by-case basis.

Procurement, properly implemented, is one of the few levers that can move EBITDA materially, quickly, and without depending on market conditions outside the operating partner’s control. A complimentary spend assessment—analyzing two portfolio companies, identifying prioritized savings opportunities, and estimating EBITDA impact—can be delivered in days, with no commitment required to proceed.

“Procurement is one of the fastest EBITDA levers available to the operating partner.” — Mark Papp, Operating Partner, Portfolio Operations & Value Creation, Tide Rock

About Mulberri

Mulberri is a Services-as-Software procurement company purpose-built for private equity portfolio companies in the $50M–$1B revenue range. Its eGPO platform combines digital purchase-to-pay workflows, cross-portfolio GPO buying leverage, managed sourcing, spend analytics and integrated payments. Operating partners can initiate a complimentary portfolio spend assessment at info@mulberri.com.

Sources: Bain & Company, ‘Welcome to a New Era in Private Equity’ (February 2026); Claymore Partners, ‘The Gathering Storm: Why Private Equity Playbooks Are Failing’ (March 2026); Mulberri eGPO Operating Partner Deck v16 (March 2026).