Turning Procurement into EBITDA — and Why More Firms Should Be Doing It

A Question for Every Operating Partner

You’ve got a portfolio of companies. Each one spends 60–80% of revenue on goods and services. Most have no procurement function, no spend analytics, and no visibility into what they’re actually paying their suppliers.

How is that not on the 100-day plan?

Every operating partner knows the EBITDA arithmetic has shifted. Bain’s 2026 Global Private Equity Report calls it “12 is the new 5” — portfolio companies now need 10–12% annual EBITDA growth to deliver a 2.5× return. With borrowing costs at 8–9%, leverage ratios compressed, and exit multiples flat, the margin for error on value creation has never been tighter.

Yet the largest cost line in the P&L — procurement spend — routinely sits below revenue growth, pricing, and headcount rationalization in the priority stack. Not because it doesn’t work. Because it’s not in the operating partner’s playbook.

This article is a challenge to change that.

The Three Objections — and Why None of Them Hold Up

We hear the same reasons from operating partners and portfolio CEOs. Let’s put them on the table and take them apart.

“We don’t have the data to make the case”

That’s the symptom, not the excuse. A spend assessment takes less than a week, costs nothing, and typically reveals that portfolio companies are overpaying by approximately 20% versus market rates. The data exists in your AP system — it just hasn’t been classified, benchmarked, or acted on. In its current state, it’s what we call ‘dirty data’, so you can’t see detail and you don’t trust it.

This is the gap between large enterprise — which has capable procurement teams, spend analytics, and sourcing tools — and the mid-market, which has none of these. Large enterprise routinely controls and optimizes spend to generate EBITDA and competitive advantage. Your portfolio companies are leaving that value on the table because nobody has looked.

“It’s not big enough to move the needle”

This is the misconception that does the most damage. Spend on goods and services typically accounts for 60–80% of a portfolio company’s revenue. If you manufacture something, your spend on materials will be high — which is obvious to most — but a tech business also has significant spend, typically on professional services and other technology. Yet this spend is rarely scrutinized with the same rigor.

At an 8× EBITDA multiple, every $1M in procurement savings creates $8M in enterprise value. On every $10M of addressable spend, we routinely deliver $800K–$1.5M in verified annual savings. That’s not marginal — that’s the single highest-return and fastest lever available during the hold period.

When you’re ignoring the largest cost line in the P&L, you’re not being conservative. You’re leaving material EBITDA on the table. It’s that simple.

“We tried a GPO or consultants — it didn’t work”

Of course it didn’t. And here’s why.

Traditional GPOs cover low-complexity indirect categories — office supplies, breakroom, basic MRO — representing perhaps 10–20% of addressable spend. They don’t touch professional services or direct spend, offer no technology platform, and provide limited, if any, spend analytics. They are reliant on suppliers to report spend volumes and fund their rebate fees. The traditional GPO model is more than 100 years old. And it shows.

Building an internal procurement function means hiring a head of procurement, sourcing analysts, and category managers. It’s a $300K–$1M annual commitment before any savings materialize, and it takes 12–18 months to ramp. It’s difficult to attract top procurement talent into an SMB — experienced professionals gravitate towards large corporates. And any new team will want procurement tools, which you then need to buy, implement, and maintain — compounding the cost before a single dollar is saved. For a $40M to $1B revenue business in a PE hold period, that timeline alone is fatal.

Consultants are a pricey option — only viable when the spend is complex and large enough to justify the outlay, which is why they tend to only work with very large portcos. A good consultant will deliver gains, but they don’t deliver any tools such as analytics and digitized processes, so benefits are rarely sustained and dissipate rapidly once they’re off the clock.

Amazon Business solves a convenience problem. It covers a few generic indirect categories with no compliance enforcement, no sourcing capability, and no visibility into total spend.

None of these options address the full scope of spend, which is precisely where the material EBITDA gains exist.

What the Firms Getting This Right Actually Do

The firms generating 3+ additional EBITDA points from procurement aren’t doing anything exotic. They’ve simply made procurement a first-order value creation workstream — alongside revenue and pricing — instead of an afterthought. Here’s what separates them.

They start with spend visibility. Top performers conduct a rapid spend assessment within the first 100 days, classifying spend by category and benchmarking against market rates — and across the portfolio. Then they address the savings potential, hard and fast. Most portfolio companies share common spend categories — SaaS, IT hardware, packaging, freight — yet these are rarely benchmarked or leveraged. The equivalent of 2 EBITDA percentage points sits unclaimed in every portco.

They leverage portfolio buying power. A single $30M–$250M revenue portfolio company has limited negotiating leverage. Aggregate that spend across five or ten portfolio businesses and the economics change fundamentally. Leading firms treat procurement as a portfolio-level capability, not a company-by-company afterthought.

They digitize the purchase-to-pay process. Manual requisitioning, email-based approvals, and spreadsheet tracking are the norm at most SMB portfolio companies — fraught with risk. Digital procurement platforms reduce purchase-to-pay costs by 30% or more, enforce compliance with negotiated contracts, and provide the spend intelligence that sustains savings beyond the initial sourcing events.

They choose outcomes over software ownership. Enterprise procurement platforms from the likes of Coupa, SAP Ariba, and Ivalua are built for Fortune 100 businesses and priced accordingly. They cost 10× more than an SMB portfolio company can justify. Leading firms are instead adopting outcome-based models — where savings fund the service — rather than sinking capital into technology that takes 12–18 months to deliver results.

The Only Lever That’s Entirely Internal

Consider what makes procurement unique. Every other value creation lever has a cost that goes beyond money.

Unlike traditional revenue and operational levers, procurement delivers fast, low-risk EBITDA gains without impacting customers, capacity, or requiring capital investment.

No customer sees it. No product changes. No service disruption. No restructuring. A dollar saved on goods and services flows directly to the bottom line.

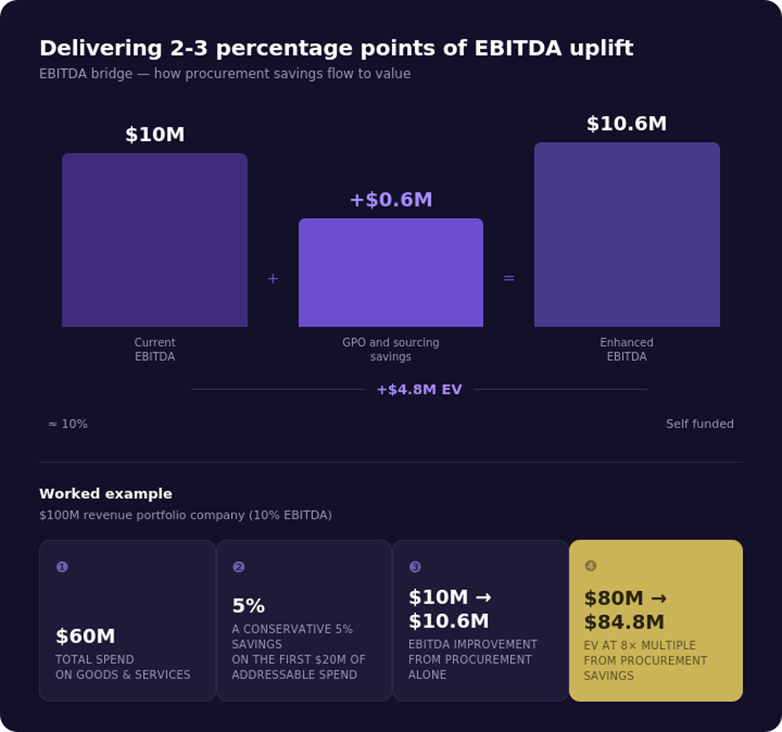

The Numbers That Should End the Debate

Consider a real-world example. A $100M revenue portfolio company with 10% EBITDA margins and $60M in annual spend on goods and services.

Procurement savings can deliver 2–3 percentage points of EBITDA uplift, translating into millions in enterprise value through sourcing, automation, and spend optimization.

These are conservative assumptions. Across 38 sourcing phase 1 events spanning three portfolio companies and $30M of addressable spend, verified savings averaged 10% — delivering $3M in annual savings. That’s a savings run rate of $250K a month.

Categories ranged from specialist components and resins to freight, packaging, and MRO. Of the $60M spend in this example, 70% or more is addressable, so you can imagine the multiples. The mechanisms range from introducing competition and switching suppliers on commodity categories, to partnering with strategic suppliers on more complex spend to mutually reduce delivery costs.

A one-size traditional GPO approach only works for simple commodity purchases, which is why a differentiated approach combining elements of what works from the traditional GPO with embedded managed sourcing services to address higher-value spend is required. Before, you might have employed consultants to hit more complex spend, but we’ve solved this with a blended platform we call eGPO.

The Operating Partner’s Call to Action

The question isn’t whether procurement can create EBITDA value. The evidence is overwhelming that it can. The question is: what’s your excuse for not doing it?

If you don’t have visibility of spend — that’s solvable in days. If you think it’s too small — you haven’t looked at the numbers. If you’ve tried a GPO and it didn’t work — you tried the wrong model.

Procurement optimization is low-risk, self-funding, fast to deploy, and — critically — wholly invisible to customers. It doesn’t compete with revenue growth or pricing strategy; it complements them. A firm that pulls the procurement lever alongside its other commercial levers creates a compounding EBITDA effect that accelerates the path to exit.

Leading PE firms have already figured this out. They understand that procurement savings are run-rate: the sooner you start, the longer the savings compound through the hold period.

The rest are leaving enterprise value on the table. Every quarter you wait is a quarter of savings you don’t get back.

Start with a Spend Assessment: Share your spend data and we’ll show you the savings potential — at no cost and no commitment.

Sources: Bain ‘Welcome to a New Era’ Global PE Report (Feb 2026); Claymore Partners ‘The Gathering Storm’ (Mar 2026); Mulberri client data.